[ad_1]

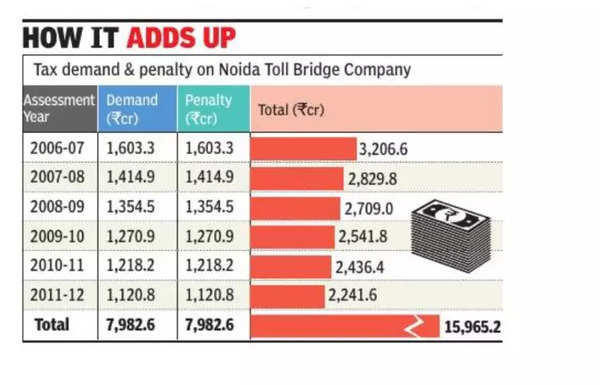

The demand of Rs 7,983 crore, and an equal amount of penalty, pertained to assessment years 2006-07 to 2011-12. While the original assessment order was issued on December 31, 2008, reassessment proceedings to disallow amortisation of interest on zero coupon bonds were initiated on March 28, 2013, which the tribunal said happened “beyond four years”. It said that for assessment year 2004-05, the issue of amortisation of interest was decided in favour of the company.

Noida Toll Bridge Company had also challenged the enhancement of the assessment by the commissioner of income tax on three counts – arrear of designated return (around Rs 180 crore), lease of land treated as revenue subsidy (Rs 1,730 crore) and disallowance of depreciation (around Rs 16 crore). The tribunal concluded that the commissioner (appeals) cannot “make an enhancement by exploring a new source of income” if the assessing officer has not assessed any income.

“… the assessing officer has never considered the three issues mentioned herein on which the CIA(A) has made enhancement, nor were they a part of the return of income. Therefore, in our considered view, the enhancement is bad in law,” the tribunal said in an order.

It then went on to dismiss the basis on which the commissioner (appeals) enhanced the assessment. The commissioner held that the company was entitled to a return of 20% from the government, which was based on a report by the chartered accountant. Noting that the certificate does not entitle the company to a return of 20% of the project cost, the tribunal noted that the commissioner (appeals) had “completely misunderstood the entire arrangement” between Noida and IL&FS and dismissed the addition of Rs 180 crore.

The commissioner (appeals) had also enhanced the assessment by Rs 1,730 crore by concluding that the land was transferred to the Noida Toll Bridge Company without any consideration to commercially exploit and this was not disclosed in the books. After arriving at the market value of the land, the remaining amount was taken to be compensation for a possible shortfall in revenue and treated as revenue subsidy for which the enhancement was made. “The lands were given on lease and, therefore, there is no question of ownership being transferred to the assessee and therefore, there is no question of any addition on this account,” the tribunal ruled.

It also dismissed the disallowance of depreciation, concluding that no capital subsidy is involved since a part of the land with the company was treated as capital receipt.

[ad_2]

Source link